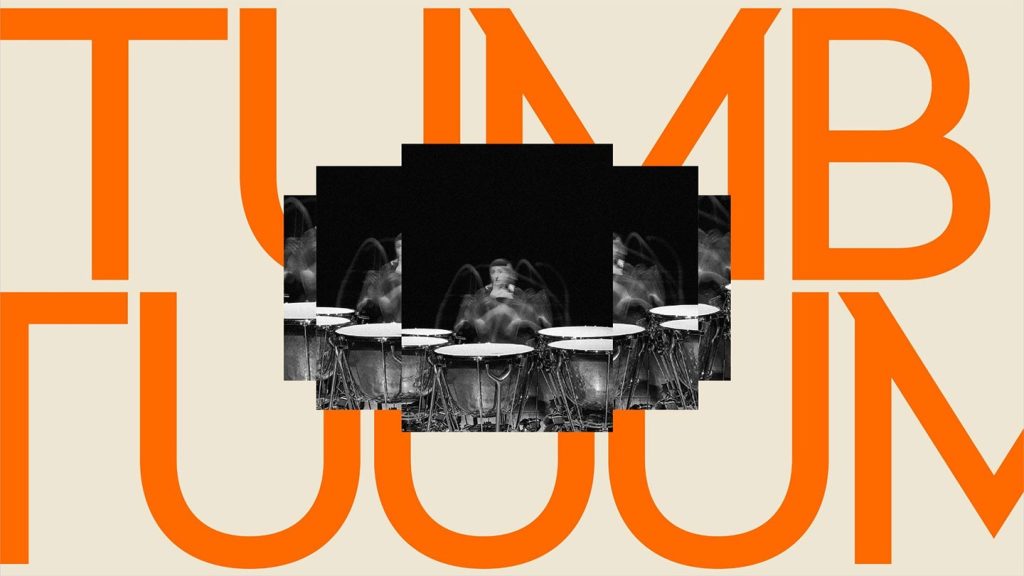

CANNES, FRANCE — In June 2024, the Milan Symphony Orchestra debuted “Growing Uptempo,” a rebrand inspired by the company’s musical core and brought to life through synesthesia. As a percussionist strikes her drums, the orchestra’s logo reverberates along with the beat. A conductor brings his music to a soft swelling, and the logo obliges in perfect harmony. A trumpeter plays a rousing tune, and the screen fills with the song’s dynamics.

“Growing Uptempo” was the fruit of painstaking work by brand consultancy Landor, which created not only the video series that launched the rebrand but also the custom fonts and overall design identity that allowed audiences to “see” the sound of the Milan Symphony Orchestra.

In an exclusive interview at the 2024 Cannes Lions International Festival of Creativity, adobo Magazine caught up with Landor Global Chief Creative Officer Teemu Suviala and picked his brain on how he and his team manage to come up with such creative ideas — especially for brands.

“[Your] brand is not one thing,” he explained. “Your brand launch is not the brand. Your brand is years of work to create moments of interaction with your audience. In the end, it’s the summary of all those moments and events that formulate the brand in the consumer’s head.”

From this perspective, the Orchestra’s rebrand built its foundation; by creating meaningful moments of interaction — both through the design itself and through the flexibility of its application — Teemu and his team were able to build multiple touchpoints in the audience’s mind.

However, building these touchpoints alone isn’t enough. To truly resonate with the audience, the message needs to have what Teemu identifies as three crucial components of creativity: empathy, curiosity, and play.

“You need to be empathetic. You need to be able to jump into other people’s shoes and understand them,” he said. “This applies to the audiences you are doing the work for, but also your collaborators, your partners, your vendors, and so on. You have to be highly empathetic.”

“The second is you need to be ultimately curious,” Teemu continued. “You have to be curious about everything. And when you’re in your audience’s shoes and if you’re curious, you can see beyond the horizon. You can see where the future could be going and be constantly asking, ‘What if?,’ and be optimistic about those what-ifs and where they can take you.”

“The last piece that is needed is playfulness, that sense of play in everything we do. Play is creativity at its best. It’s no rules, everything is allowed. You’re testing, you’re prototyping, seeing where things go. You’re making mistakes. You just have to watch kids play and take inspiration from there.”

That deep understanding of what makes creativity resonate is exactly what makes efforts like “Growing Uptempo” work. In a marketing landscape where branding needs to be more multisensorial than ever, it’s this trifecta of empathy, curiosity, and play that will help brands continue to surprise and delight audiences.

Or, as Teemu put it: “Good ideas either make you uncomfortable, or they make you smile. And great ideas do both.”

CANNES, FRANCE — This is Part One of a series where Game On captain Rey Tiempo analyzes the winners from this year’s Cannes Lions Entertainment Lions for Gaming category, through the lens of an advertising industry veteran AND a hardcore gamer.

Note that some of this year’s winners have already been featured in a previous Achievement Unlocked segment, especially the work from this year’s D&AD. This new series will see picks from work that made their awards circuit debut in Cannes.

THE EVERYDAY TACTICIAN by Xbox / McCann

The Gaming POV

The never-ending quest (that seems to be winding down to an end sooner than we think – more on this later) for the video game experience is to get as close to reality as possible. Yes, of course the settings may often be fantastical, characters may seem totally otherworldly, situations may be utterly disparate from everyday experiences, enough to support the need for escapism. But the essential elements that make a world “work” are all still based on known realities that we humans operate under. The physics particularly are still based largely on the laws of our physical world (with our own takes, manipulations, creative licenses, etc.).

Most especially, this pursuit of reality is most evident in the evolution of video game graphics, with the advancement in technology getting better and better at dialing up visual fidelity (sometimes, it even gets TOO real, to a point where gamers now ponder, “Is too much graphical realism what we really want in games these days?”) Sports and simulation games definitely operate under reality-inspired gaming experiences (I remember feeling like I could really dunk my way to the ring ala Double Dribble’s awesomely-lowres cut scenes), and they’ve only gotten better through the years, with more mindblowingly-detailed graphics (“Hey, I can now see hi-res sweat!”) and more-engaging-than-ever-before gameplay.

I realize that is one looong intro to the point I wanted to make. But a necessary setup to this brilliant Grand Prix-worthy work from Xbox. See, while games get better at mirroring the real world, this idea mirrors the mirrored games back to reality. It’s as simple as a creatively groundbreaking idea can get (all winning gaming ideas are simple at their core, made complicated by ad agency bosses who disappointingly don’t understand gaming, but I digress.)

A gamer, who has honed his skills in running video game teams in Football Manager (a game that so realistically mirrors the experience in the real world) has been tapped to take his gaming skills back to the real world and help a very real world club get promoted to the very real EFL. It’s a crazy loop of gaming-reality convergence that totally deserves all the merit it has been earning. In a huge way, this reminds me of a similar success story of that one avid Gran Turismo gamer who eventually earned his way to race in real world racing cars, in real world circuits (the film this story is based on is an absolute blast and an underrated gem in the history of video game-related adaptations.)

The work is also a great demonstration of a winning gaming case formula: proving or disproving what gaming can or cannot do. Xbox, through the years, has been giving us some of the best examples: that gaming can help education (“Field Trips”); that game worlds can be tourist destinations (“The Birth of Gaming Tourism”); that gaming can bridge generations (“Beyond Generations”); and they can add this latest one, that gaming skills can help you land real world jobs.

Most definitely a worthy year two top prize for the Cannes Lions Entertainment in Lions Gaming category. It’s a creative gaming idea that amplifies the authentic gamer experience and celebrates it in the most authentically rewarding way. One of the best examples of a true Gaming X Marketing work that exemplifies how gaming solves problems it sometimes doesn’t even know it can.

Year Two Jury President Lydia Winters of Mojang(far right). Photo taken last year, during the year one judging of the Cannes Lions Entertainment Lions in Gaming category. Judging with Lydia was Philippines’ own Joey David-Tiempo (second from left, right next to the author). Also in the photo, Dentsu Creative ECD Gary Amante (back) and Bean Tiempo (third from left).

The Advertising POV

A winning gaming case made stronger by all the traditional advertising media content it has spawned. From the documentary film series, to social, news coverage, to all of the unpaid and organic gaming and football fan-related content around it. As a way to bring in more players for the game (and to sell more copies of course), there is no better selling strategy than to actually prove the effectiveness of your product’s selling point. It’s probably one of the best pure product demo advertisements out there in recent years that’s endemically in the gaming space.

The campaign title itself is a stroke of genius – the “everyday” gamer who has honed his skills by playing “every day” has been elevated into a masterful tactician, a story that’s clearly not as “everyday” as it appears. And yet it can be, for the thousands of “everyday” gamers who can now play this game (“the most played Football Manager ever”)… well, “everyday.”

ABOUT GAME ON

Rey Tiempo is a Creative Gaming Brand Specialist. A hardcore gamer since childhood, Rey is multi-awarded creative gaming marketer, with accolades from the world’s biggest creative industry award shows. A veteran creative head with over 25 years’ experience, Rey leads the Gaming and Marketing conversation in the Philippines and Asia, as Founder of “Game On,” the first and only ad industry column and portal on Gaming X Marketing, and as Founder and Chief Creative of Co-Op Play, a team of Brand Gamification Specialists. Currently playing: Black Myth: Wukong; Kunitsu-Gami

Dennis Nierra is a Creative Director at BBDO Guerrero.

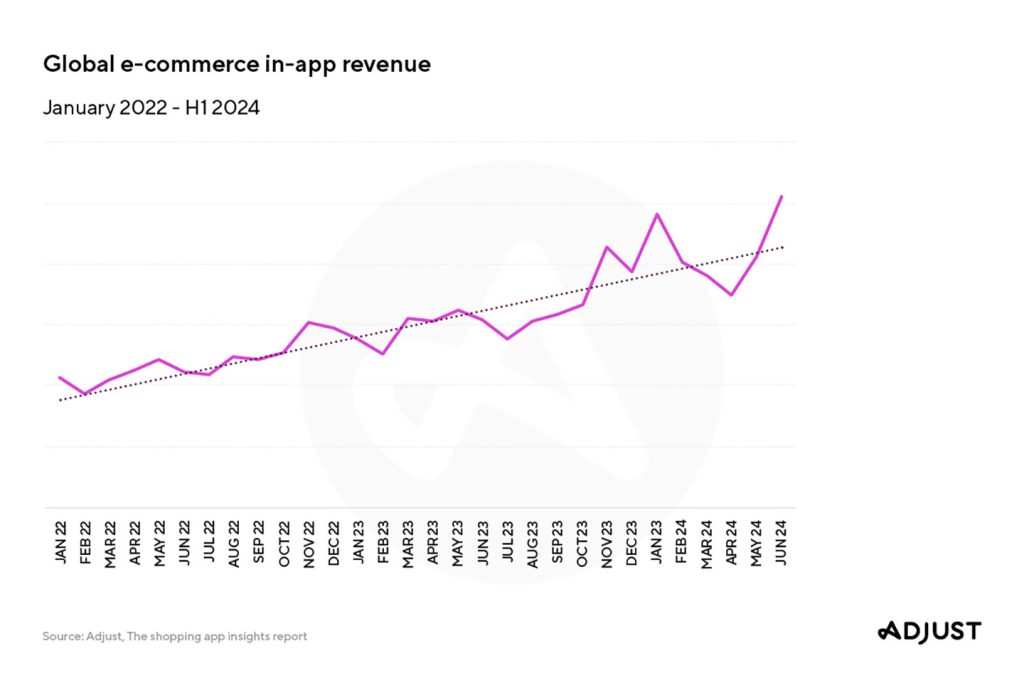

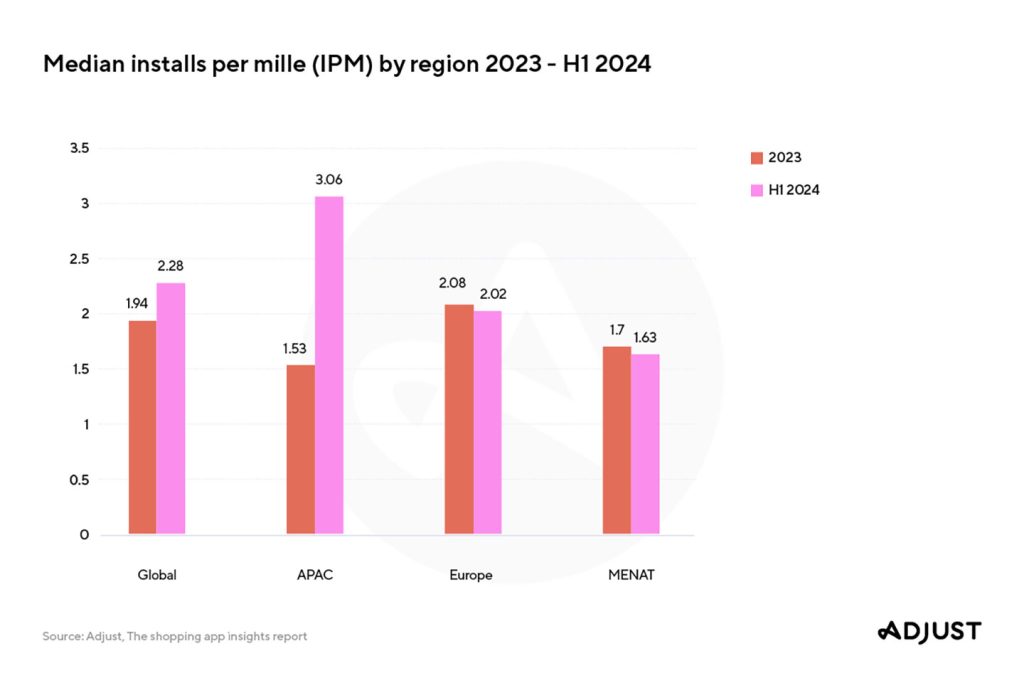

SINGAPORE — Leading measurement and analytics company Adjust released “The Shopping App Insights Report” to prepare mobile marketers for the Q4 shopping season and beyond into 2025. Surpassing the overall vertical’s average, shopping app installs rose 61% YoY (year-over-year) in H1 2024, while installs of e-commerce apps overall climbed 25% and sessions rose to 13% YoY. This growth comes as retail media networks continue to scale, next-generation digital shopping experiences are deployed and mobile wallets become commonplace.

“Shopping apps are transforming how consumers interact with brands and make purchases,” said Tiahn Wetzler, Director, Content & Insights at Adjust. “By working with AI and Augmented Reality, and integrating dynamic channels like social commerce and CTV, marketers can enhance user engagement and create experiences that drive high conversion rates.”

Marketers should take note of the Q4 shopping season, which results in big install increases. In a 2023 survey by InMobi in Asia, 73% of respondents in Indonesia, Singapore, and the Philippines plan to do a mix of in-person and mobile shopping. Adjust recorded installs 40% above the daily average on October 17, 2023, and 41% higher on October 18.

Adjust’s shopping app insights report provides e-commerce app marketers and developers with key insights across all key sub-verticals. Highlights include:

E-commerce app session lengths in e-APAC averaged 10 minutes, a slight decrease from the global average of 10.5 minutes. However, the region had a 15% Day 1 retention rate compared to North America and LATAM, which had rates of 11% and 14.4%, respectively.

APAC had the highest number of partners per app, rising from 10.7 to 11.8 from 2023 to H1 2024.

In-app revenue for e-commerce apps increased 36% YoY with 60% of in-app revenue coming from Android devices globally. The biggest spikes in 2023 occurred in Q4, with November revenue 34% higher than the monthly average and December up 22%.

Global median installs per mille (IPM) rose from 1.94 in 2023 to 2.28 in H1 2024, indicating improved ad campaign effectiveness. APAC saw a significant increase from 1.53 to 3.06.

“In a competitive market where engagement and customer loyalty are critical to moving the bottom line, staying at the forefront of intergenerational consumer expectations – and the technologies behind them – is paramount,” continued Tiahn. “As the shopping app landscape evolves, scalable growth will be achieved through a strategic channel mix, smart personalization, and a data-obsessed approach to measurement and analytics.”

“As shopping habits rapidly change with evolving e-commerce technology, it is highly valuable for marketers and retailers to sharpen their campaign strategies to ensure optimal growth and success, especially in APAC,” says April Tayson, Regional Vice President for INSEAU at Adjust. Our data shows that several Southeast Asian countries, such as Indonesia, Malaysia, Philippines, Singapore, and Vietnam, spend a considerable amount of time within apps, posing an opportunity for businesses to ride on this trend, which will likely grow even further in the foreseeable future.”

For additional findings and analysis, download the full report here.

MANILA, PHILIPPINES — At a time when countless movie and TV titles are on offer via streaming and video-on-demand platforms, when anything anyone wants to watch is at their fingertips, format programs — such as variety, reality, and talk shows — remain highly popular. While Filipinos enjoy tear-jerking drama, heart-pumping action, and gut-busting sitcoms, they also get their kicks from singing, dancing, contests, and games.

Some of the most enduring local programs are format shows, like Eat Bulaga, which just celebrated its 45th anniversary. Its veteran hosts, Tito, Vic, and Joey, are still some of the most famous and well-loved “artistas” in the country. It’s no wonder, then, that when TV5 acquired the top-rating noontime show, loyal TVJ fans followed it to the Kapatid channel.

A track record of breakthrough, brandable entertainment

Although Eat Bulaga is quite new to TV5, the station is not at all new to the genre. Unlike other networks, where narrative series dominate, TV5 has long been producing iconic format shows, such as Wow Mali and Tropang Trumpo, which brought much joy to Filipino homes decades ago.

More recently, TV5 successfully launched other innovative programs, like the now-concluded SpinGo and Barangay Singko Panalo. For both economic reasons and sheer entertainment value, Filipinos are magnetically drawn to gamified television with prizes, and these two were made that much more compelling by their breakthrough, never-been-done-before concepts. The truly pioneering SpinGo was the first game show to inextricably merge TV viewing with in-app play. And the highly relatable Barangay Singko Panalo glorified the core unit of the Pinoy community, the barangay, by setting the games in ultra-familiar environs, populated with “common tao” characters.

For viewers who prefer a magazine talk show format, Güd Morning Kapatid has segments covering an array of topics and hosts who represent a range of ages and interests; thereby appealing to a broad audience and lending itself well to various branded features. Currently, TV5’s strongest proposition is Wil to Win, which has a slew of brandable executions for on-air and on-ground, through which brands can reach Willie’s legion of avid fans. Like with SpinGo, technology enhances the reach and viewing experience of Wil to Win, thanks to the online livestream.

By using original, homegrown concepts versus foreign franchises, format shows satisfy Pinoys’ taste for comedy and game shows, while offering advertisers a way to strengthen their relationship with their target market.

Engaging and flexible content

The spontaneous, unscripted, often interactive nature of these programs means that they resonate more strongly with audiences and invite active engagement with them. TV5 Vice President of Sales for Entertainment & News, Sheila Aligora-Balcueva, avers, “Format shows will always have its space in the landscape, providing a unique flavor and energy to the TV viewing experience. Though they are equally engaging and compelling, I’d say narratives are a more passive & lean-back kind of content, whereas variety and game shows are lean-forward, asking you on different occasions to vote, think, participate, and play to win.”

In addition, programming that is locally conceived and tailored to the culture, language, and preferences of the viewers not only ensures authenticity, but also lends relevance to the brands that are part of them. And since these shows allow for a lot of flexibility — from product intrusion, to segment sponsorship, to innovative and immersive branded experiences — they provide a multitude of opportunities for brands to increase their affinity to consumers. “Format shows easily render themselves to content integration, whether via customization of existing portions or the creation of totally bespoke executions. We can be more direct with branded executions here and need not tiptoe around the suspended reality of narratives,” Balcueva explains. And she promises that there will be much more to expect from TV5: “More formats tapping the pulse of pop culture and entertainment, whether innovations or reboots of classic TV5 offerings.”

Solutions for diverse tastes and needs

With the ever-widening variety of programs available today, it makes sense to cater to different tastes, beyond the usual narrative series. Because format shows delight and excite Pinoys, while at the same time providing a wealth of possibilities for brands to make an impact on their target market, TV5 will continue to offer them—for both viewers’ and advertisers’ happiness. As Guido Zaballero, President and CEO of TV5 Network Inc., says,“The free-to-air business is not exclusive to one player. We are all finding solutions that address the diverse needs of our clients. TV5’s strategy is to create format titles for our audiences to love and embrace as part of their lives.”

Learn more about TV5’s shows and latest news on tv5.com.ph

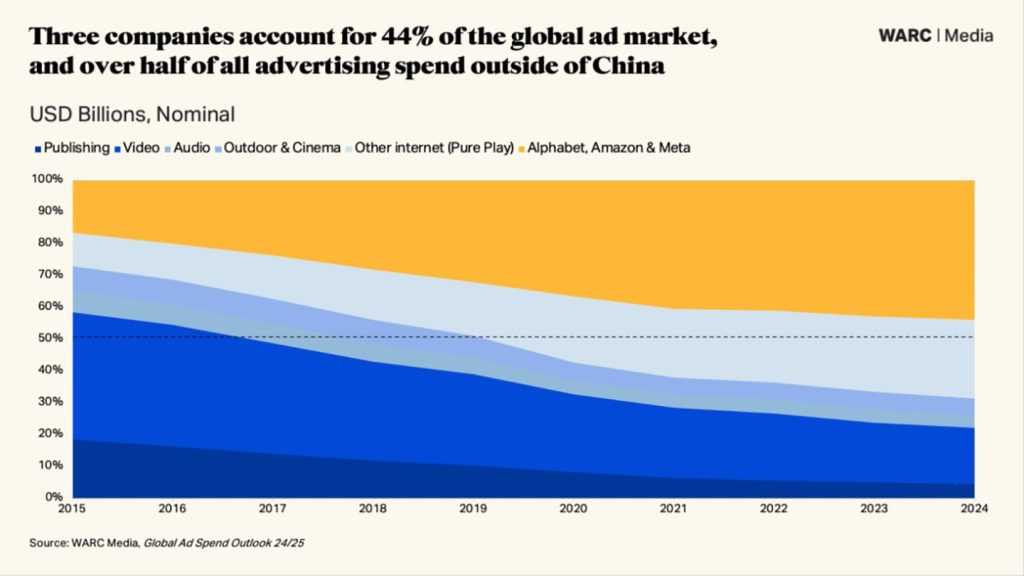

LONDON, UK — A new study from WARC, the experts in marketing effectiveness, has found that global advertising spending is on course to grow 10.5% this year to a total of $1.07 trillion — the best performance in six years if the post-Covid recovery of 2021 (+27.9% year-on-year) is disregarded.

Ad spend growth is also anticipated next year (+7.2%) and in 2026 (+7.0%), culminating in a global ad market worth $1.23 trillion. Global ad investment has more than doubled over the last decade and has grown 2.8x faster than global economic output since 2014. Just three companies — Meta, Amazon, and Alphabet – account for more than 70% of this incremental spend. This trifecta is expected to attract 43.6% of all advertising spend this year, rising to a share of over 46% by 2026.

WARC’s latest global projections are based on data aggregated from 100 markets. New for this edition, WARC is now leveraging an advanced neural network machine learning model that projects advertising investment patterns based on over two million data points spanning macroeconomic data, media owner revenue, marketing expenses from the world’s largest advertisers, media consumption trends, and media cost inflation. It is believed to be one of the most comprehensive advertising market models available to the industry today.

The new projections show that “pureplay” (i.e. online only) internet companies are set to record a 14.0% rise in advertising revenue this year, reaching a total of $735.7 billion. In total, almost nine in every ten (88.5%) incremental dollars spent on advertising this year will go to online-only businesses, with half (52.9%) being paid to Alphabet, Amazon, and Meta. Taken together, pureplay platforms are set to account for over 70% of all advertising spend worldwide next year.

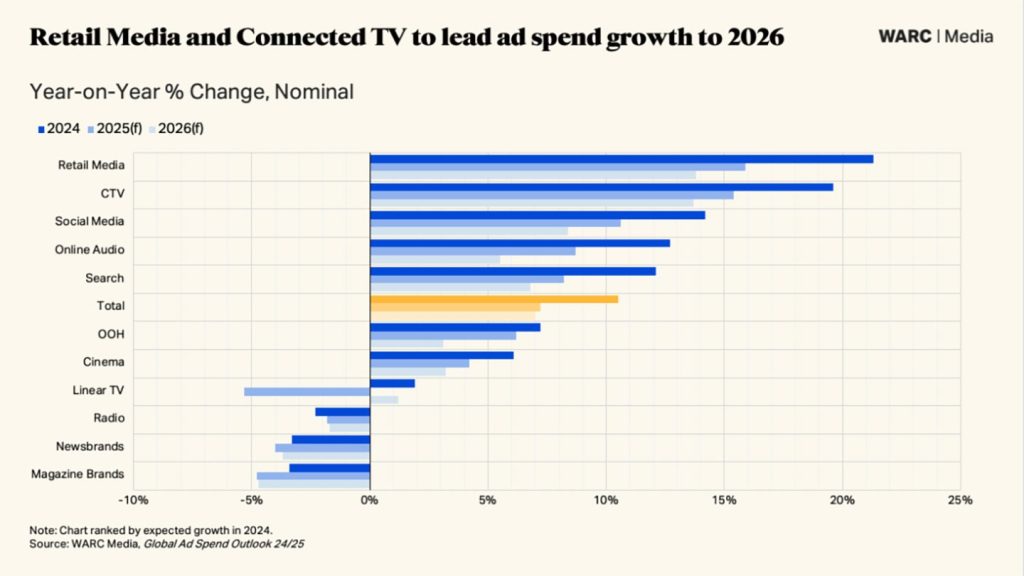

Retail media (+21.3%), social media (+14.2%), and search (+12.1%) are set to lead digital growth in 2024, with these three sectors alone accounting for over 85% of online spending and almost three in every five (58.7%) incremental dollars spent on advertising worldwide this year. All are benefiting from the increased adoption of AI-driven ad services and growing appreciation of first-party data.

James McDonald, Director of Data, Intelligence and Forecasting, WARC, and author of the research says: “The global ad market has doubled in size over the last decade, with advertising investment growing almost three times faster than economic output since 2014. Three companies — Alphabet, Amazon, and Meta — have been the largest beneficiaries from this period of expansion, attracting seven in ten incremental ad dollars over the last ten years.

“With retail media expected to lead ad spend growth over the coming years, and with new, diverse players emerging in ad selling — from Uber to Chase — we are once again seeing the value of first-party data in targeting the right person with the right message at the right time. Such data, combined with new AI enhancements, will constitute the fabric of the advertising industry for the next decade and beyond.”

Key findings outlined in WARC’s Global Ad Spend Outlook 2024/25 are:

MEDIA TRENDS: Global ad spend is forecast to rise 10.5% this year to a total of $1.07 trillion, and then 7.2% in 2025 and 7.0% in 2026; social, retail media and CTV to lead growth

At $241.8 billion in 2024, social media is the largest single advertising channel measured in WARC’s study, overtaking search (excl. retail media) for the first time last year. It accounts for 22.6% of all global ad spending this year and is forecast to rise to a share of 23.6% by the end of 2026.

Within social, Meta is the largest individual player, commanding 62.6% of the market this year. Its share is being eroded however, most notably by Douyin and TikTok owner Bytedance, which now draws a fifth (20.1%) of all social spending, up from a share of just 9.3% five years ago. TikTok is on course to account for over half of its parent company’s advertising revenue for the first time next year with estimated ad billings over $28 billion, though uncertainty remains around the platform’s future in the US — its largest market by far with 170 million monthly active users.

The main social platforms have reported a fillip from new, AI-enabled services during the first half of 2024, a trend set to underpin the advertising industry at large in the coming years. Over half of all AI-enabled spend — defined as involving some form of recommendation algorithm, natural language processing, or search optimization – today occurs in the social media sector.

Search advertising (excluding retail media) accounts for 21.8% of global advertising spend, at a forecast total of $223.8 billion this year. Its share has consistently grown since WARC began monitoring the sector in 2013, though it is set to plateau in 2026 as more purchase journeys begin in retail media environments and social commerce begins to realize its potential outside of Asia. Another potential headwind may be the rise of AI-driven search, and uncertainty around what the ad experience will look like for consumers more familiar with text-based search experiences.

Google accounts for more than four-fifths (84.0%) of the global search market, with its paid search revenue set to top $200 billion for the first time next year. Google’s share rises to over 90% if China is excluded, a position of dominance which this month led a US judge to rule the company in breach of antitrust laws.

Retail media is expected to account for 14.3% of global ad spend this year — a total of $152.6 billion — which is double the share recorded in 2019 before the pandemic contributed to an exceptional growth spurt. Indeed, retail media is expected to be the fastest-growing channel over at least the next three years.

Amazon is the dominant global player, with anticipated ad revenue (excluding Twitch and Prime Video) of $55.9 billion equivalent to more than a third (36.6%) of all retail media spend and over two-thirds excluding China this year. While competition is heating up, such billings eclipse the near $4 billion, Walmart is due to net in 2024, and the $1 billion ad business Uber is building, while Amazon is also due to have surpassed Alibaba by ad revenue for the first time this year.

CTV is on course to be worth $35.3 billion to advertisers this year, roughly a quarter of the size of the linear TV market. Growth is rapid; CTV spending is expected to rise 19.6% and is set to account for two-thirds of all growth in the video (linear + CTV) market this year, and all growth in 2025. By 2026, CTV is projected to account for almost a quarter (23.9%) of all video ad spend, at $46.3 billion.

Netflix is the largest streaming provider globally, with 277.6 million subscribers worldwide in Q2 2024. However, its global advertising business is unlikely to grow too far beyond $1 billion this year. YouTube’s ad income – which we do not yet classify as CTV – is expected to rise 14.3% to $36.0 billion this year. Further, YouTube’s ad revenue is set to top $45 billion globally by 2026, almost as much as the entirety of the global CTV industry at that time.

Legacy media, encompassing print publishing, broadcast radio, linear TV, cinema, and out-of-home (OOH), now collectively account for a quarter (25.3%) of total advertising spend, having recorded a dip in share in each of the last 15 years.

Advertising spending on legacy media is expected to total $270.5 billion this year, representing a 1.5% rise from 2023. Much of this growth can be attributed to US political spending; with this removed legacy media are, collectively, set to record a 0.5% decline in advertiser investment in 2024.

Linear TV spending is expected to grow by 1.9% this year, its best performance since 2014 if the post-Covid recovery year of 2021 (+12.7%) were excluded. The market is flat (+0.1%), however, excluding US political spending. Out-of-home (+7.2%) and cinema (+6.1%) will see some growth this year, though radio (-2.3%) is expected to record its third consecutive year of decline. Newsbrands (-3.3%) and magazine brands (-3.4%) are also due to see losses across print and online editions.

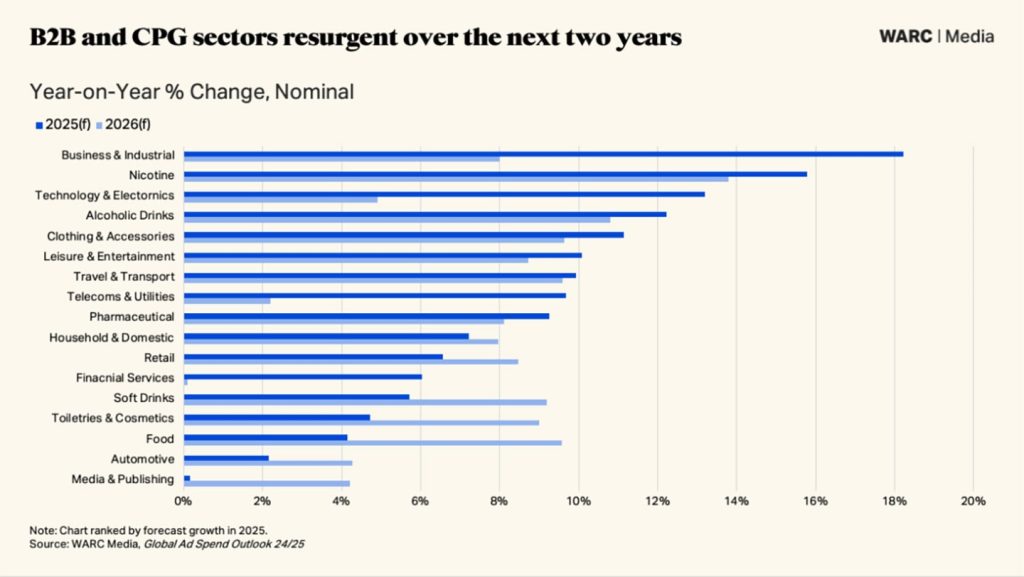

PRODUCT SECTOR TRENDS: Technology & Electronics (+13.2%), Alcoholic Drinks (+12.2%) and Clothing & Accessories (+11.1%) the fastest-growing consumer sectors next year. US political spending is expected to reach $15.8 billion this year; over a fifth is spent on socials.

Advertising spending during the 2024 US presidential election is on course to top $15 billion for the first time, with an expected total of $15.8 billion up by over 40% on the previous cycle in 2020. Spend had been lagging the 2020 total earlier this year, but the surprise decision to change the Democratic candidate has led to an influx in spending to reposition the new ticket of Kamala Harris and Tim Walz. This shift is perhaps most pronounced online: political spending on social media is tracking 27.4% higher in Q3 2024 versus Q2 2024, with social spending by both main parties on course to reach $3.6 billion this year.

Retail — the largest of the 19 categories monitored by WARC — is anticipated to record a 2.5% dip in global spending this year. Our definition of this sector is broad, however, ranging from quick service retail (QSR) to grocery to department stores to online retailers, such as Temu. The latter is expected to continue investing heavily in advertising, particularly in Europe this year, but it is an exception — the longer tail of retailers are facing business pressures from soft consumer demand.

Technology & Electronics – the third-largest product sector monitored by WARC – is expected to post the fastest growth this year, with incremental spending of $17.0 billion worldwide. The sector had recorded declines in advertising spend in both 2022 and 2023, as central banks raised interest rates sharply in an attempt to stymie inflation, exposing over-leveraged tech startups in particular.

Technology & Electronics (+13.2%), Alcoholic Drinks (+12.2%), and Clothing & Accessories (+11.1%) are forecast to lead ad spend growth among consumer-facing products in 2025, though Business & Industrial, the second-largest category, is expected to be the fastest-growing category overall next year (+18.2%), as budgets unlock during a period of comparatively favorable economic and trading conditions.

The Nicotine category is also growing rapidly, albeit from a low base; it is the smallest of the 19 product categories monitored by WARC at $13.0 billion in 2024. Spend is set to grow 56% over the three years to 2026 — reaching a total of $17.2 billion — driven almost entirely by vape products which skew heavily towards online advertising.

REGIONAL TRENDS: North America to grow 8.6% this year to $348 billion, APAC growth cools to just 2.0% owing to a stronger dollar, Europe is forecast to rise 5.0% to $164.9 billion, while Middle East ad markets are largely unaffected by looming threat of regional conflict

North America is on track to be the fastest-growing region this year — inflated by the US presidential elections — with ad spending rising 8.6% to a total of $347.5 billion. US ad spending is expected to grow 8.9% this year (+4.0% excluding political spend, more than double the 1.4% growth rate recorded in 2023) to a total of $330.8 billion. A further rise, of 3.6%, is forecast next year, by when the US ad market should be worth over $342 billion. The Canadian ad market is due to grow 7.5% to $16.8 billion this year.

Latin America (+6.2% to $32.1 billion in 2024) then follows, with its largest market, Brazil, forecast to record local currency growth of 9.6% this year to a total of $14.8 billion — an acceleration from the 7.5% rise recorded last year. Our forecasts suggest that online advertising will account for over half (50.4%) of the Brazilian ad market for the first time this year.

APAC’s (+2.0% to $272.0 billion this year) largest market – China – is projected to see ad market growth of 6.4% this year to RMB1.32 trillion ($181.2 billion), an easing from the 9.3% rise recorded in 2023 as consumer demand remains soft and economic expansion lags stubbornly behind the target. Pureplay Internet will account for over 86% of the Chinese ad market in 2024, though social media (+10.5%) and retail media (+8.2%) will expand at a slower rate this year than last.

When measured in local currency — to exclude the distorting effect of exchange rate fluctuations — we see that India will be the fastest-growing key market this year, with advertiser spending rising 11.9% to INR1.08 trillion ($12.8 billion).

Japan — the fourth-largest ad market in the world — is forecast to grow by 5.2% this year to $36.9 billion, though this equates to a 6.3% decline when measured in US dollars due to the Yen falling to a decade-long low. Australia’s ad market is expanding by 2.0%, a modest but welcome change of fortunes following flat (+0.3%) growth in 2023, while Indonesia is expected to achieve 7.8% growth this year.

Advertising spending across Europe is forecast to rise 5.0% this year to $164.9 billion. The UK, the largest European market by spend, is expected to post an 8.0% rise to $47.5 billion in 2024 per market data from the AA/WARC Expenditure Report. On the European mainland, France (+8.0%), Italy (+5.4%) and Germany (+4.0%) are all expected to see healthy gains this year, with the former in particular benefiting from increased advertising activity around the Paris Olympics and Paralympics in the third quarter.

Brand spending in the Middle East and Africa is currently on course to rise by 4.2% to $12.6 billion this year, though fortunes are mixed. African spending is expected to be flat (+0.2%), following a 15.7% decline in 2023 and a 1.4% dip in 2022. South Africa, the region’s largest market, is expected to see its ad market grow 6.0% this year but this translates to a 1.1% increase when measured in dollars owing to a weak Rand by historical measures. Ad spending in the Middle East is set to rise 8.1% this year but that is subject to change should conflict spread beyond Gaza to the wider region.

A complimentary article by WARC’s James McDonald, author of the report, is available to read here. WARC subscribers can read the article and access additional data here.

MANILA, PHILIPPINES — Breaking the status quo is akin to the moment when the first primate mastered fire or when someone boldly decided to try eating eggs for the first time. These breakthroughs arise from the “uncomfort zone,” a space where the unconventional, unexpected, and unusual are birthed.

At the 4th General Members Meeting on August 06, VML Manila’s Chief Creative Officer Joe Dy emphasized the importance of this “uncomfort zone” in creative work, stating, “It isn’t for everyone, but it is an important space in our line of work.” His words suggest that while human nature often gravitates toward familiar patterns, true innovation demands that creatives consistently push beyond the comfort of the known.

“The uncomfort zone is a place I’d like to describe where great ideas really happen. This is actually where the unusual is the usual. It’s where the crazy ones play.”

While relating that it entails ruffling feathers and stirring the pot, Joe chalked it up to these factors, explaining how to get out of the rut and not return to what’s predictable and, therefore, boring.

Subverting expectations

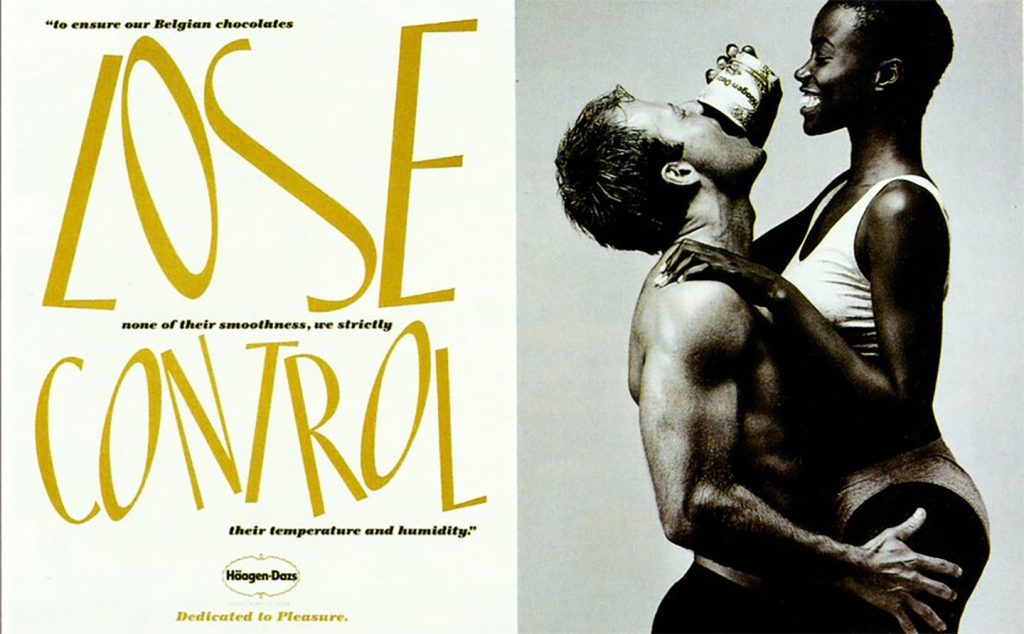

Turning off what you perceive as correct can help you frame your mind to subvert expectations. “By turning off this switch in our heads, it helps us unblock creative pathways and explore unfamiliar things,” Joe said, referencing Haagen Dazs and Philip Morris’ early campaigns as examples. These brands not only took bold steps but also successfully changed consumer behavior toward their products.

“Don’t do it in the way you’re expected to do.”

When everyone else was selling ice cream, Haagen Dazs sold sensuality. When Marlboro was the cigarette for women, Leo Burnett introduced the cowboy image to market it to male consumers.

“It’s all about subverting expectations; subverting expectations of the market, the category, the client, and the audience. And sometimes, even your own expectations.”

When wrong becomes interesting

“Sometimes, correct can be boring. It’s safe, it’s wallpaper, it’s stock, but when you get it wrong, wrong is actually interesting. Why are we always dismissing wrong all the time?”

Being category wrong, brand voice wrong, and market wrong, although a gamble, can pay off. “Every category works in their best practices,” he said but in the cases of Crest, and P&G, it proves otherwise.

“You can’t change the game if you keep playing by the rules,” Joe asserted. Drawing from his extensive career and experiences, he underscored that success doesn’t always come from following the conventional path. In recent years, several unconventional approaches—what some might call “wrongs”—have proven the validity of Joe’s advice, with the results speaking for themselves.

Many of today’s cultural norms have emerged from challenging and reshaping traditions. Take Santa Claus, for instance. Before Coca-Cola’s iconic advertising campaigns, the jolly, red-suited figure we now associate with the holiday season lacked a consistent image.

Similarly, until De Beers Jewellers revolutionized the perception of engagement rings with copywriter Frances Gerety’s iconic tagline “A diamond is forever,” diamonds were not the default choice for symbolizing eternal love.

“Sometimes you have to invent a culture if the culture that you want to influence isn’t there,” Joe shared.

Question reality and indulge the impossible

In maintaining correctness, blinders prevent looking at things in a fresh light. The antidote? Dare to be stupid, ignore sanity, and go a little nuts.

“Logic is what everybody sees,” Joe prefaced, “Don’t let logic keep you from making magic.”

From smashing together what is bizarre to inter-species muppet pairing, there’s no denying what meshing things off-center can do.

“When the unusual succeeds, it becomes the usual.” In the instance of Leo Burnett UK’s 2001 campaign, an edible billboard showed that any food indeed tastes supreme with Heinz Salad Cream. This execution inspired many brands, including McDonald’s, Carlsberg, and Thornton Chocolates.

As one of his favorites, Joe played Samsung’s “Do What You Cant” campaign, which encapsulates his points.

Responsibility in pulling things off

It’s not about being reckless. It’s about gutting it out.

Ultimately, ruffling feathers and stirring the pot should not be self-serving. Staying grounded, he said that there are things that can’t be done for a reason, and it lies on the “dinosaurs in the room” (himself included) to have the wisdom to know when to push for the idea.

“You can’t just be different for difference’s sake. Otherwise, you can be self-indulgent, and that is the danger. It still has to be in the service of a business objective.”

“Braving that comfort zone can be scary, but it can be fun. It can be very, very rewarding not just in awards but also in financial benefits for our clients.”

Closing his talk and the members meeting, Joe posed the challenge: Isn’t it time we stop following best practices and return to creating best practices?

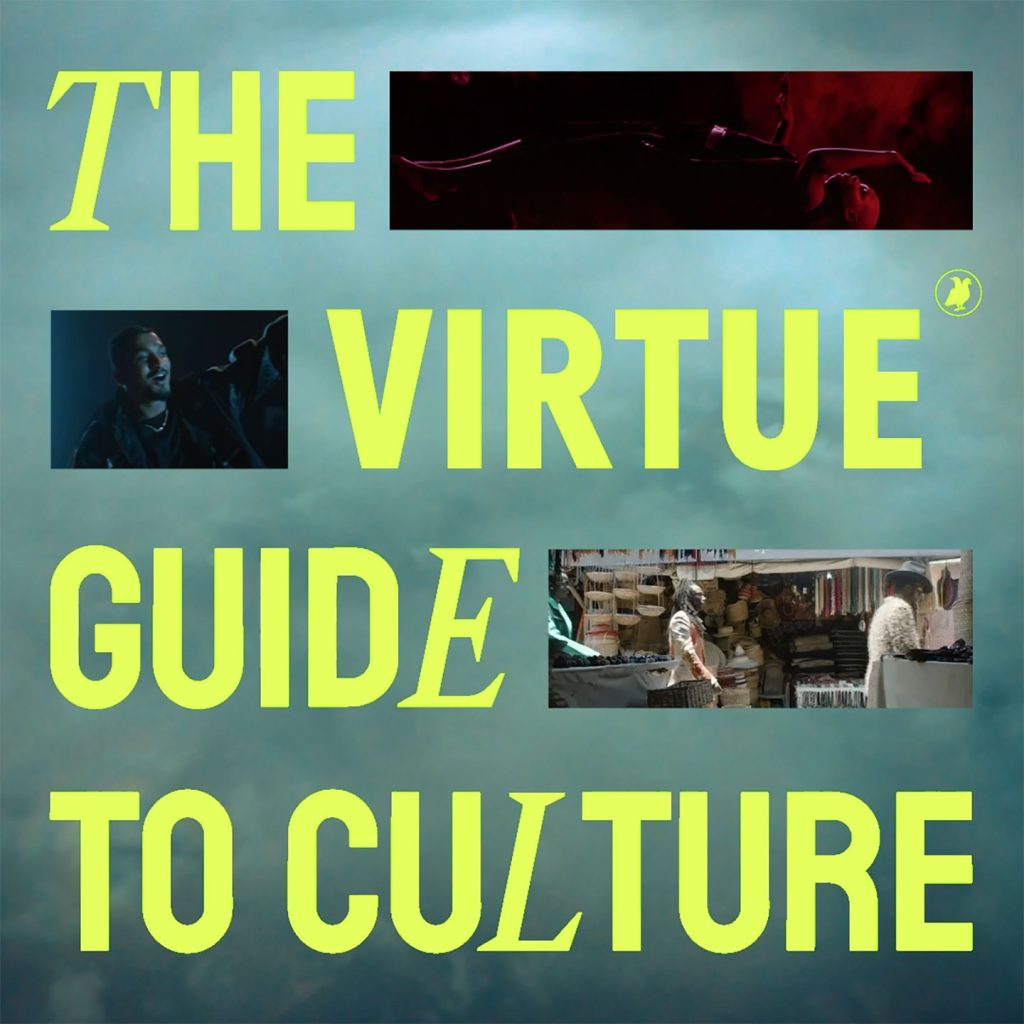

MUMBAI, INDIA — Virtue Worldwide, the creative agency powered by VICE Media Group, unveils the “2024 Virtue Guide to Culture.” This in-depth report, embedded in culture, sheds light on the critical codes guiding Gen Z and their behaviors. The propriety research was conducted across key APAC markets, including India. Leveraging insights from VICE Media’s global community of 40,000 young people, as well as its extensive network of journalists and content creators, the guide offers a comprehensive analysis of the emerging cultural codes influencing Asia’s Gen Z.

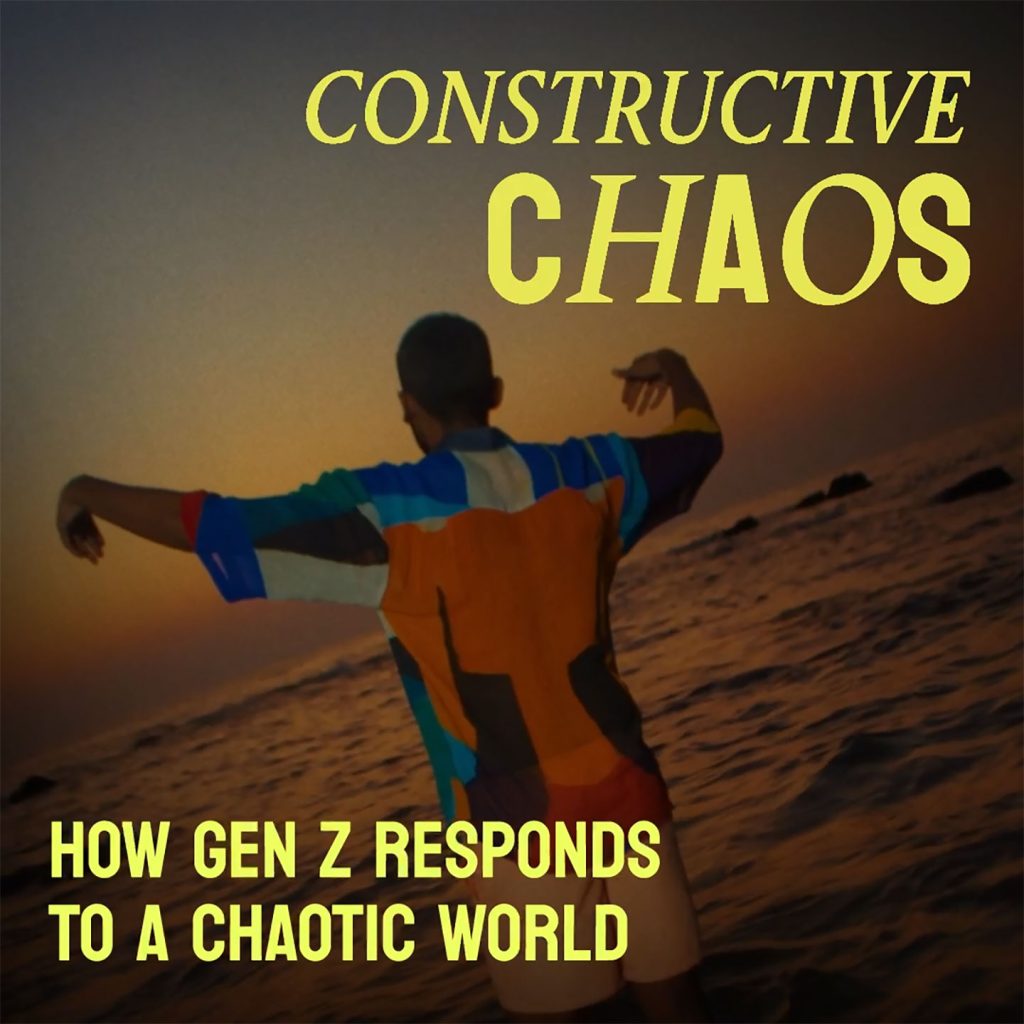

Cultural Code #1: Constructive Chaos

Asian youth is turning chaos into a wellspring of inspiration and self-expression. By channelling the power of the weird and absurd through art, technology, fashion, and culture, that is amplified by social media. This expression is truly coded in uniqueness and breaking conventional norms. The emergence of a generation that embraces eccentricity and authenticity is revolutionary in India, which has been a traditionally conformist society, where fitting in and adhering to prescribed standards of success have long been the norm.

Absurdity is the ultimate definition of authenticity in this new world order. 86% of young people say, “It’s normal to be weird,” with cringe content becoming mainstream in India. Homemade, lo-fi, and slapstick social content is gaining popularity, standing out from polished feeds and celebrating authenticity. Unlocking of this weirdness paves the way and creates room for infinite expressions of self.

Cultural Code #2: Fan Authority

Fanpower rises from a deep-seated desire to belong. It gives a sense of community and a collective identity. Power has shifted to the fans, who can make or break celebrities. They have become pivotal in shaping the success of public figures.

Take cricket, for instance. Fans in India have had a deep, entwined, long relationship with the game and its players. During the recent T20 World Cup, emotions ran high against Hardik Pandya, who was believed to be out of form. Ridicule, brickbats, and social media memes became central, but with his significant contribution to a subsequent win, he redeemed himself for his fans and Indian cricket.

Fans have also expanded beyond the sphere of celebrities to champion their causes and push for independent initiatives.

Cultural Code #3: Empathetic Technology

Technological advancements are reshaping intimacy and social interaction. 31% of youth agree AI will provide therapy within 10 years, and 62% of young Indians believe AI will moderate social media within the next decade.

KamaSutra’s “Kamaverse” is a prime example, offering a virtual space for open and positive discussions about sex. Virtual avatars in “Kamaverse” answer questions without judgment and provide virtual rooms for product discovery in a safe and private environment, helping young Indians become more open-minded and communicative partners.

Cultural Code #4: Feminism’s Soft Revolution

Laughter, leisure, and reclaiming spaces to move and walk are emerging ways of assertion and protest, in the feminist movement. Changing the world while having fun is the new code. Whether it is reclaiming streets by meeting to sleep in parks or midnight walks, these are brave, bold, new ways to protest and assert presence.

Saumya Baijal

A viral video featuring Arundhati Roy’s “militant laugh” symbolizes this brave and playful assertion of presence. The movement champions the power of being oneself and making impactful changes while reveling in the journey. Women are braver, bringing in change and sparking conversations that matter in the gender movement.

Reflecting on the implications of the research for the Indian market, Saumya Baijal, Strategy Lead, India at Virtue Worldwide, said,“For brands to have conversations with audiences that matter to them, it is critical for them to seat themselves in culture codes relevant to those audience groups. The Virtue Guide To Culture unlocks such codes that can enable communications that can be both short term, specific and dynamic, as well as long-standing and consistent.”

SYDNEY, AUSTRALIA — A new study by R/GA Australia, an advertising company leveraging technology and creativity, has highlighted a critical flaw in how current digital experiences are built: they are still tailored to “Digital Adopters” rather than “Digital Natives.”

“The Gen One Report,” the first-of-its-kind research, draws from insights from over 1,500 Australians aged 15 and above, using diary studies, in-depth interviews, and quantitative analysis. It explores the digital divide of expectations and how they should dramatically transform how we design digital interactions.

The report’s findings center on how the digital landscape has been shaped for and by “Digital Adopters,” individuals who were not born into the digital world but have adapted to it over time. This has led to direct translations of physical experiences into the digital realm and decades of incremental innovation.

Shifting design priorities is imperative to adapting to the changing demographic landscape dominated by “Digital Natives.” R/GA’s research shows that adhering to outdated design approaches risks alienating Gen One, who have elevated expectations of technology. Interestingly, the research suggests that by designing for this group, everyone can benefit from it. This approach ensures no one is left behind while advancing everyone forward, recognizing Gen One as the first generation in a new digital age.

This is particularly important as our daily digital tools — such as apps, websites, and government services — are currently designed with Digital Adopters in mind rather than catering to the Digital Natives shaping the landscape today.

Re-thinking digital design

From digital literacy to digital empathy, key findings include:

Gen One’s optimism and anxiety: Digital Natives are optimistic about technology’s potential to enhance their lives yet are more likely to be worried about the negative impacts on their well-being compared to Digital Adopters.

Content consumption and well-being: Gen One prefers short-form, easily consumable content. However, this can contribute to feelings of anxiety and distraction. They seek a balance between technology’s benefits and drawbacks.

Privacy, trust, and ethical concerns: Establishing trust between governments and Australians is vital in the age of emerging technology. Digital Natives, though accustomed to online information sharing, have major concerns about how government data is handled. They worry about security gaps and demand more robust assurances for their credentials, stressing the importance of better trust-building practices.

Strategies for engagement

Multi-generational design architecture: Moving from vertical to horizontal service structures is important to support individuals effectively when needed. Gen One’s preferences vary by life stage, requiring tailored features and tactics to cater effectively to these different stages.

Hedonic and emotional design: Moving beyond standard UX best practices, there’s a need to include enjoyable and emotionally impactful elements in digital interactions to create not only seamless but meaningful experiences.

Hyper-personalization and gamification: Moving from creepy to cool, connected services should provide people with all the services they need with minimal friction. Digital Natives thrive on personalized and gamified content; tailored experiences incorporating achievement-oriented elements can help maintain their interest and trust. And ultimately drive the positive behaviors that government and brands are ultimately measured by.

Tish Karunarathna, Executive Director of R/GA Public Practice, added, “We set out to understand what makes Gen One different, so everyone can benefit from a digital-first world. Persisting with a Digital Adopter-centric design approach risks alienating Gen One and limiting technological adoption. It’s time for us to learn from Gen One to accelerate toward a more inclusive digital future.”

Victoria Curro, Managing Director of R/GA Australia, said, “Australia’s largest demographic is the one that’s never known a world without the internet. We have to evolve the user experience to address the expectations of a generation born with technology, and in doing so we’ll create a more inclusive and accessible future for everyone.”

SINGAPORE — MSL Asia Pacific has released the latest Women’s Forum Barometer, Asia Pacific, which brings together recent research, disaggregated data, and responses from citizens across 10 different countries, with a focus on Australia, China, Japan, and Korea. This edition reveals today’s complex reality and persistent stereotypes of working women, comparing respondents from the G7 nations to those in Asia Pacific (Australia, China, Korea, and Japan).

This edition of the Women’s Forum Barometer, Asia Pacific, highlights the ongoing differing perceptions and experiences between women in the G7 and the APAC:

Roughly 49% of respondents from Asia-Pacific endorse the stereotype suggesting inherent disparities in natural aptitudes between men and women, perpetuating the notion that men excel in scientific subjects while women excel in literary subjects;

Respondents in Asia-Oceania agree more strongly than those in the G7 that women “can’t have it all, if they want to be a good mother, they have to accept to partly sacrifice their professional career” (60% compared to 48% in G7); and

Alarmingly, close to half of the surveyed women have had to take breaks from their careers for at least a month to fulfill caregiving obligations, a scenario notably less common among men (47% compared to 28%).

“As we navigate through the evolving landscape of gender equality, it is crucial to still recognise that Asian women face unique challenges distinct from those experienced in G7 countries. Addressing these inequalities requires a concerted effort to rethink and reshape our gender policies, while simultaneously challenging and transforming outdated cultural norms. By doing so, we can pave the way for a more equitable and inclusive future for women across the Asia Pacific region,” said Margaret Key, CEO of MSL APAC.

“The Women’s Forum Barometer highlights the disparity between perception and reality for women in the workplace. It is important to understand that empowering women in the workplace goes beyond creating opportunities; it also involves reshaping perceptions and challenging the realities they face daily. By doing so, it will pave the way for women to thrive and lead, transforming not just the workplace but society as a whole,” said Nannette Lafond Dufour, Chief Impact Officer at Publicis Groupe.

Stereotypes about women in the workplace

Out of all respondents, 71% of women felt they have more opportunities to succeed than men with equal competency, highlighting a 12% gap, with only 59% agreeing.

Of the 51% of total respondents — encompassing all age groups and genders combined — who believed that “Career-wise, men are naturally more ambitious than women,” 55% were men.

Within the 42% of all men and women who agreed that “Women are psychologically more fragile than men,” men made up 45% of those convinced.

Working at the sacrifice of their private life

Gender stereotypes persist, especially among the working population. 70% of respondents are convinced that “It is more difficult for a woman than for a man to have a successful career because she has to accept to partly sacrifice her family life”

However, there seems to be a slight shift in the value of professional careers in a woman’s life, as only 38% of respondents agree that “A woman will always be happier in her role as a mother rather than in her professional life.”

Within the 4 Asian countries investigated, inequalities within the labour market are a reality in the lives of women

The four countries experience a larger gender pay gap: 20.9% as compared to 12% in OECD

Women are less present in the labor market at 56.9% as compared to 71.5% of men

More women work part-time: 32.9% compared to 13.5% of men

Despite equal or higher qualifications, women are often paid less

Clear perceptions of inequalities in careers

One in 3 women have already realized they were paid less than male colleagues with equal competence

One in 3 women have realized that a male colleague had been promoted or chosen for a promotion over them, even though she was more competent

Inequality hides under the cover of unpaid work

Globally, women contribute significantly for all unpaid care. If this current trends continue, the gender gap in unpaid care work will not be closed until 2228

The inequality and unpaid care results in career breaks with major negative consequences on women’s careers and financial security: 47% of respondents stopped working for one or more months to be able to care for loved ones; 42% for one or more years for the same reason. This is compared to 28% and 22% of men respectively for the same reason.

In the European Union, women over 65 have a gender gap in their pension income of 37.2%. Across OECD countries, the average elderly poverty rate is 15.7% for women, compared to 10.3% for men.

The Key Role of paternity leave in closing the gender gap

In Australia, fathers receive 2 weeks, paid at 43.2% of salary

In Japan, fathers receive up to 52 weeks, paid at 61.3% of salary

In Korea, fathers receive up to 54 weeks, 46.7% of salary

The stark gaps between paternity leave in these markets highlight main issues such as part time and temporary workers being excluded from such benefits, the stigma and fear of career impact that discourages leave usage, and the low compensation which reduced financial feasibility

To combat these inequalities, concrete calls to action have been tested and received strong support.

Education and STEM: 82% of respondents support the inclusion of an equal number of female and male role models in STEM textbooks; 79% of respondents support the inclusion of mandatory training on unconscious gender biases in the academic curriculum.

World of work and business: 74% of those questioned are in favor of disclosing the names and companies where there are salary gaps between men and women with equal skills; 765 of respondents support the requirement of companies to publish an index (score out of 100) showing wage gaps.

Family: 84% of respondents support businesses providing quality and affordable childcare and elder care; 74% of those surveyed are in favour of reserving part of the parental leave for exclusive and non-transferable use by fathers.

Overall, stereotypes about women in the workplace are more pervasive in the Asia Pacific region, as compared to G7 nations. Significant efforts have been made to address the gender gap and reduce the burden of unpaid work on women, but more needs to be done.

Despite the workforce segmentation, there is broad and growing support from both genders, industries, and governments, signaling a collective commitment to drive the necessary to effect changes.

MANILA, PHILIPPINES — Artificial intelligence holds the potential to reshape journalism in Southeast Asia. A new Vero survey reveals that journalists recognize the growing importance of AI in their work and believe deepening their understanding of this technology is crucial.

The study, “AI and Journalism in Southeast Asia: A Survey of Opportunities and Challenges,” provides a detailed analysis based on a survey of 75 journalists in Indonesia, the Philippines, Thailand, and Vietnam.

AI is setting a new precedent for how news is gathered, stories are told, and information is consumed. “AI’s influence on journalism extends beyond just automation; it’s about enhancing the accuracy, speed, and depth of reporting,” said Raphael Lachkar, COO of Vero. “As pioneers at the intersection of communications and technology, we are committed to leading this transformative journey, helping our clients and partners not only adapt but excel in this AI-driven era.”

Embracing AI across borders:

In Indonesia and Thailand, 95% of journalists have a significant understanding of AI, with Thailand also showing a 95% adaptation rate, reflecting effective integration into their work.

In the Philippines, 90% are familiar with AI, but only 52% have integrated it into their work.

Though 78% are familiar with AI in Vietnam, 100% expressed positive attitudes toward adapting to AI’s impact on their work.

Journalists expressed valid concerns about AI, including its governance, impact on labor, and cybersecurity issues, particularly in Thailand, where there’s an apprehension about overreliance on AI potentially compromising the quality and trust in journalism. “In Vietnam, the enthusiasm for AI is tempered with a keen focus on strong data privacy and security measures,” Raphael added.

The need for tailored AI education is clear. Journalists across the region are eager to fully grasp AI’s capabilities to maintain competitiveness in a rapidly evolving digital media landscape. Vero recommends the following steps to foster a positive AI integration:

Educate: Develop and provide tailored training programs to facilitate seamless AI integration into journalism.

Acknowledge: Address concerns of seasoned journalists about AI’s impact on job security, copyright, and the integrity of journalism.

Be Transparent: Clearly communicate the functionalities and limitations of AI tools to build trust and manage expectations.

Be Responsible: Maintain a robust support system to address any challenges presented by AI tools, ensuring accountability and ethical usage.

“We envision this white paper as a catalyst for ongoing research and proactive engagement on AI’s role in enhancing journalism, ensuring it serves the public good while respecting the fundamental principles of the field,” said Chatrine Siswoyo, Vero Senior Advisor for ASEAN.

The white paper on “AI and Journalism in Southeast Asia” is available for free on the Vero website, and is offered as a resource for communications and media professionals navigating the AI landscape.